OPEN ENROLLMENT from November 1st to December 15th for a January 1st start date

There are many significant changes for 2026. Please read this entire blog post for the most direct and up to date information and how it may impact you. Feel free to reach out anytime if you have any questions. If you have questions for us please call or text 425-802-2783, email us at [email protected] or schedule a time on our calendar.

YouTube Video of Individual Health Insurance changes for 2026

SCHEDULE A TIME ON OUR CALENDAR HERE

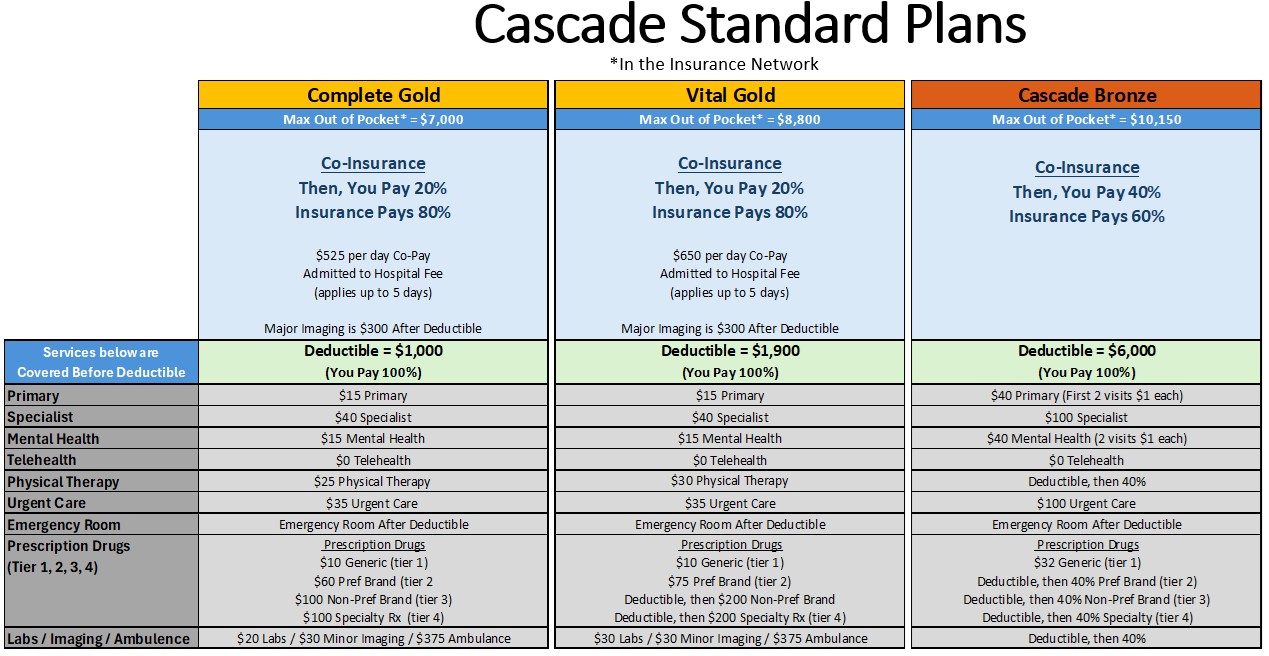

- For 2026 the Gold plans will be cheaper than the Silver plans. You heard this correctly. The largest change is that ALL Silver plans are going up approximately 40% for 2026. This was done on purpose by the WA Exchange so those getting tax credits get 40% more tax credits. In practice, what they are trying to do is get people to buy a Gold or Bronze plan and pay much less than you would have otherwise. We generally recommend those to get a “Vital Gold” a Complete Gold plan” or a “Cascade Bronze plan”. The “Cascade Silver” plan is intentionally overpriced as it is the baseline for calculating tax credits.

- For those of you on a SILVER plan, in general you are most likely going to be automatically moved to the “Vital Gold” plan, yet please double check on your own. This is a good thing and lower cost as well. Win/Win.

- All Bronze Plans on the WA Exchange are now HSA (Health Savings Account) eligible. If you purchase one of these plans, you can contribute additional tax-deductible dollars to a separate HSA checking account. For 2026, the single-person limit is $4,400 per year, or for a Household, the limit is $8,750. If you are between the ages of 55 and 64, you can contribute an additional $1,000 per year per household. This money is tax-deductible and pays out tax-free for ONLY qualified medical expenses (excluding monthly premium payments). We cannot provide accounting advice, so please consult with your tax preparer to determine if this is correct for your specific situation.

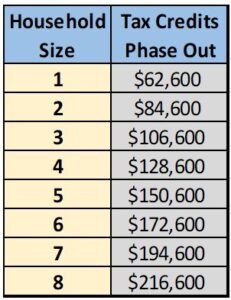

- TAX CREDITS: If you are reading the news, the “Enhanced Premium Tax Credits” are phasing out at the end of the year. If you are of moderate income, you may pay the full price for health insurance in 2026 based on your income and the size of your taxable household. Here is a chart that shows where the tax credits phase out for the size of your taxable household for 2026.

- For those of you on a REGENCE plan, there is a dramatic change in their network. See the Regence comments below.

NOTE: Our company Achieve Alpha Insurance is now part of Heffernan Insurance Brokers. We are still the same amazing people providing great service, just part of a larger company now. Just like when someone gets married they are the same person, yet their last name changes.

Below is a summary of the changes and price increases for the carriers in 2025: The good news is that there are very few changes if any with some carriers, which is great for consistency.

Average Rate Increase in 2025 = 21%

- AM Better = 27%

- Cascade Gold 8%, Cascade Silver 42%, Cascade Bronze 23%

Regence = 10%

- Cascade Gold -4%, Cascade Silver 45%, Cascade Bronze 5%

Premera = 15%

- Cascade Gold -5%, Cascade Silver 43%, Cascade Bronze 17%

LifeWise = 12%

- Cascade Gold -6%, Cascade Silver 36%, Cascade Bronze 15%

Kaiser Permanente = 10%

- Cascade Gold 5%, Cascade Silver 32%, Cascade Bronze 4%

United Healthcare = 38%

- Cascade Gold 14%, Cascade Silver 59%, Cascade Bronze 25%

Molina Marketplace = 28%

- Cascade Gold 18%, Cascade Silver 48%, Cascade Bronze 24%

Below is a brief commentary on the carriers and the network changes

AM Better: The good news is that they will still be the lowest-cost provider, as they are increasing slightly less than the average plan. Those getting tax credits should see prices stay about the same. No real changes in the networks for the most part. Overall, AM Better is a great carrier; however, it may not be ideal if you require a mental health provider, a dermatologist, or access to a variety of independent doctors. They have a moderate network of independent doctors, which is why they offer a lower-cost plan compared to Premera and Regence, with costs often half of those of their competitors.

NOTE: For 2026 the AM Better Bronze plan has moved to the “Cascade Select” network which is the “Public Option” with a super small network. DO NOT PURCHASE THIS PLAN, the NETWORK is much smaller! If you are being moved to the “AM Better Cascade Select BRONZE” plan please upgrade to the “AM Better Vital Gold or AM Better Complete Gold” or chose another insurance carrier. You have been warned. They do not cover many doctors at the regular hospital networks, mainly community health centers.

Regence: Most carriers are increasing premiums by a significantly greater amount than Regence in 2026. However, their hospital network has changed significantly (mainly in the greater Seattle area. Regence will now mainly cover ONLY Swedish & Providence in the Seattle area and will NOT cover University of Washington, Evergreen, Overlake, Virginia Mason, or MultiCare. It’s a nearly complete switch from prior years, as they previously covered almost all the hospital systems, but now only cover Swedish & Providence. One positive note is that Regence will cover Polyclinic (which is part of Optum). Regence has in-network coverage in WA, OR, ID, and Utah.

Premera: At this point, the Premera plans are so expensive that the only reason to stay on this plan is if your expensive medication is covered better here, or you have ongoing medical issues that you need to see specific doctors. Still a good carrier, but the only remaining customers are those who utilize a significant amount of medical coverage. Premera Individual plans will cover Swedish/Providence, UW, Evergreen, Overlake, Virginia Mason, CHI, and MultiCare.

LifeWise: The good news with LifeWise is that it is not changing its network, so most things will remain similar, and it is a good option overall. LifeWise is owned by Premera, yet it mainly covers only Swedish, Providence, and CHI Franciscan systems (excluding the old Virginia Mason facilities). Both LifeWise and Regence will have a similar hospital network for 2026.

United Healthcare: UHC is increasing in price more than everyone else, yet it is still cheaper than Premera. They are best if you mainly want to go to Polyclinic, as the only other carriers they accept are Premera and Regence. They have a much larger network, covering most of the hospitals, including the University of Washington, Virginia Mason, CHI, Evergreen, Overlake, and MultiCare. The network for psychologists and independent doctors is good, yet Premera and Regence are probably slightly larger individual doctor networks. Overall, UHC has a good network; however, it is also as expensive as Premera, Regence, and LifeWise.

Kaiser Permanente: Kaiser is an HMO system where you must go to Kaiser facilities unless you need to go to an Emergency Room. Since Kaiser does not have its own hospital system, it allows you to go to any hospital for emergencies; however, you still need to visit their facilities for regular and specialist visits. Overall, the Kaiser plans are not cheap, as they are on the higher end of the cost spectrum for plans. You would mainly keep Kaiser if you also want to visit other Kaiser facilities in-network in California, Oregon, Colorado, Hawaii, and Virginia.

Molina Marketplace: Molina is a low-cost carrier similar to Ambetter, but slightly more expensive. They both have a moderate network of independent doctors. The primary reason to choose a Molina plan is if you wish to visit Valley Medical Center in Renton or University of Washington facilities, as AM Better does not cover these hospital systems. NOTE: Molina Marketplace plans do not cover ANY medical expenses outside the USA. All other carriers have emergency coverage outside the USA. You can always purchase a travel plan, but they often have limited coverage. If you plan to be outside the USA for a significant amount of time, you should probably choose another carrier.

SCHEDULE A TIME ON OUR CALENDAR HERE

Gary Franke, Tamara Chandler, Brianna Crawford & Melissa Tibbs

Heffernan Insurance Brokers

Individual Health & Medicare Specialists

1100 Bellevue Way NE, Ste 8A-545

Bellevue, WA 98004

425-802-2783 (call or text office line)

[email protected]

www.wahealthplan.org